Advantages of Defined Benefit and Cash Balance Plans for Independent Doctors and Small Medical Practices

- These IRS-approved qualified plans provide for the largest annual contributions to retirement plans, often exceeding $150,000 annually on behalf of the physician.

- All contributions and fees for these plans are tax deductible in the year they are paid.

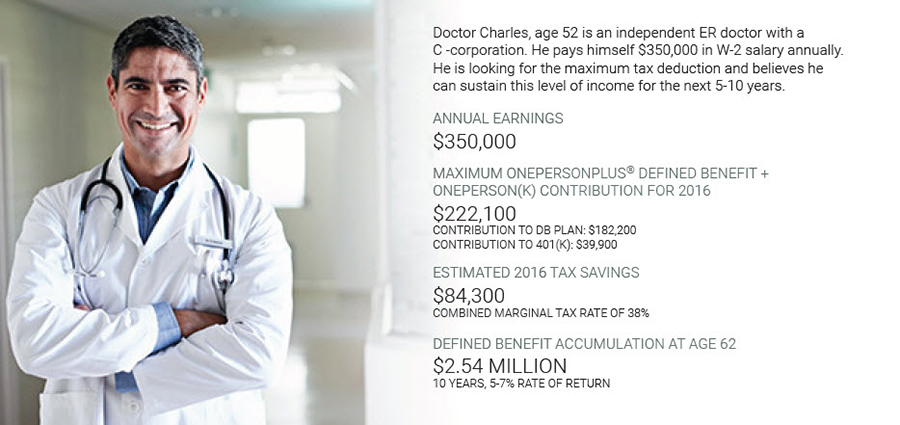

- Starting as late as age 52, a physician earning $265,000 can accumulate $2.6 million in 10 years.

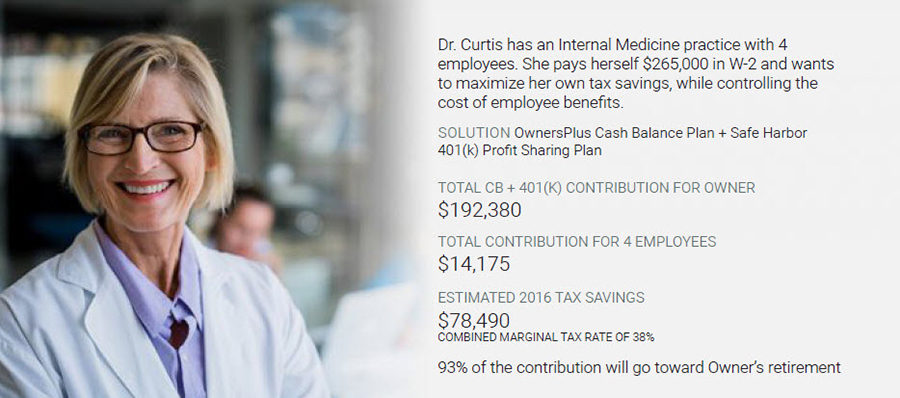

We partner with advisors who provide financial and tax consulting for physicians, dentists and small medical practices. Traditional Defined benefit plans work best for the solo practitioner or doctor with spouse or family practices. When a medical practice includes common law employees, we recommend our OwnersPlus™ Retirement Program which combines a Cash Balance Plan with a Safe Harbor 401(k)/Profit Sharing Plan.

Special Considerations for Physicians and Small Medical Practices

- The older the physician, generally, the higher the contribution. Most physicians begin their practices with school debt and incur high expenses to set up a practice. As practices mature and they are older – 45+ — they have the excess cash flow to support high contributions and need the tax deductions.

- Doctors who are employed by hospitals or research centers generally will participate in a retirement plan through the institution. However, many of them have side income from independent research studies, serving as expert witnesses, sitting on board of directors, etc. This secondary income source may not be needed to maintain life style and can be used to fund a defined benefit plan and reduce the tax liability.

- Doctors who work as locum tenans – serving temporarily in hospitals or other locations — often receive high self employment income for these engagements and have few work-related expenses. Some doctors choose to do this as a way of semi-retiring. Generally, the net profit from this income can be used to fund a defined benefit plan if it is not needed for current cash flow.

- If the physician owner of a medical practice adds a spouse who works in the business to payroll, this could increase the total contribution for their family in a situation where otherwise, the doctor would have maxed out with only his or her own contribution.

Contact us today to discuss how we can assist you!